Weekly Market Update – 15 September 2025

- Stefan Lubek

- Sep 15, 2025

- 3 min read

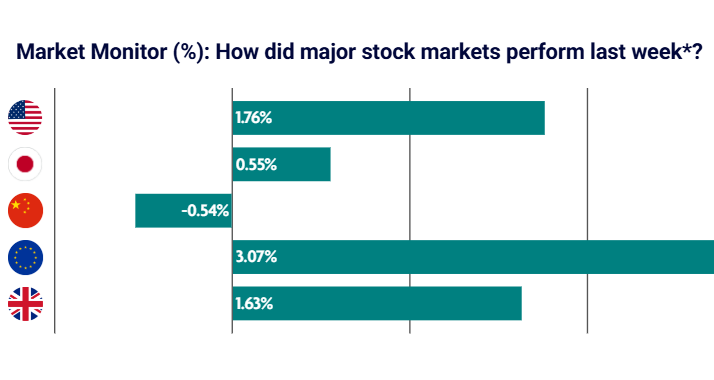

A strong week for global equities driven by expectations that the U.S. Federal Reserve is likely to cut interest rates at its upcoming FOMC meeting. Japan was the standout performer, with the market reacting favourably to the announcement that Prime Minister Shigeru Ishiba intends to resign.

US: Stocks rally to record highs amid rate cut expectations and AI optimism

Most major U.S. stock indexes finished the week higher ahead of the Federal Reserve’s September 16-17 monetary policy meeting, at which the central bank is widely expected to lower short-term interest rates. Enthusiasm surrounding the ongoing artificial intelligence (AI) boom - supported by Oracle’s announcement of a substantial guidance increase amid several large new AI deals - also helped lift major indices. Consumer price growth accelerated in August, according to data released by the Bureau of Labor Statistics (BLS) on Thursday. The agency’s consumer price index (CPI) data showed headline prices rose 2.9% year over year in August, an increase from July’s reading of 2.7%. Core CPI, which excludes food and energy costs, rose 3.1% over the same period. The BLS also reported that its August producer price index (PPI), a separate measure of inflation that gauges price increases at the wholesale level, unexpectedly decelerated to a 2.6% year-over-year increase versus 3.1% in the prior month.

Japan: Equities gain on announcement that Prime Minister Shigeru Ishiba intends to resign

Japan’s stocks rose over the week, as markets appeared to take in stride the announcement by Prime Minister Shigeru Ishiba that he intends to resign, following sizable losses in two general elections within the space of 12 months. His ruling Liberal Democratic Party will now hold an emergency leadership election on October 4, with investors likely focused on whether Ishiba’s successor adopts a more expansionary fiscal approach, potentially including cuts to income and consumption taxes. There was some speculation that heightened political uncertainty could lead to a delay in further monetary policy tightening by the Bank of Japan (BoJ), but many investors continued to converge around the view that the central bank could still raise interest rates this year, as the economy and prices develop in line with its forecasts.

China: Bullish sentiment among retail investors drives equities higher

Mainland Chinese stock markets rose as bullish sentiment among retail investors persisted. Ample domestic liquidity - as opposed to improving corporate earnings or economic data - has fuelled a rally in China’s stock markets since April as cash-rich households seek higher returns amid low interest rates and a lack of better investing options. Recent advances in artificial intelligence have also boosted sentiment. On the economics front, data showed that deflationary pressures continue to weigh on China’s economy. The producer price index fell 2.9% in August year on year, marking the 35th straight month that the gauge has remained in negative territory, but narrowed its decline from July’s 3.5% drop.

Europe: European stocks rise amid expectations that the U.S. Federal Reserve is poised to lower interest rates

Major stock indexes rose for the week, with Italy’s FTSE MIB climbing 2.30%, France’s CAC 40 Index advancing 1.96%, and Germany’s DAX adding 0.43%. The European Central Bank (ECB) held its key deposit rate at 2%, as expected. ECB President Christine Lagarde reiterated that the Eurozone was “in a good place” with inflation at 2%. The central bank also slightly raised its forecasts for inflation and economic growth this year, which financial markets interpreted as a signal that the current rate-cutting cycle was over. The ECB now projects 2.1% inflation in 2025 and 1.7% in 2026 and expects the economy to expand 1.2% this year compared with its previous estimate of 0.9% growth.

UK: UK equities gain for the week despite data pointing to a stalling economy

The UK’s FTSE 100 Index gained 0.82% for the week, despite data pointing to a stalling economy in July. Equities were lifted by expectations that the U.S. is likely to cut interest rates this month. UK gross domestic product (GDP) was unchanged in July, after growing 0.4% sequentially in June. Services and construction expanded marginally, but broad-based weakness in manufacturing - which shrank a greater-than-expected 1.3% month over month - offset the gains. The rolling quarterly rate slowed to 0.2% from the prior 0.3%. Chancellor Rachel Reeves has made growth her “number one mission”, but the economy has lost momentum in recent months.

Comments