Weekly Market Review - 29 June 2026

- 13 hours ago

- 4 min read

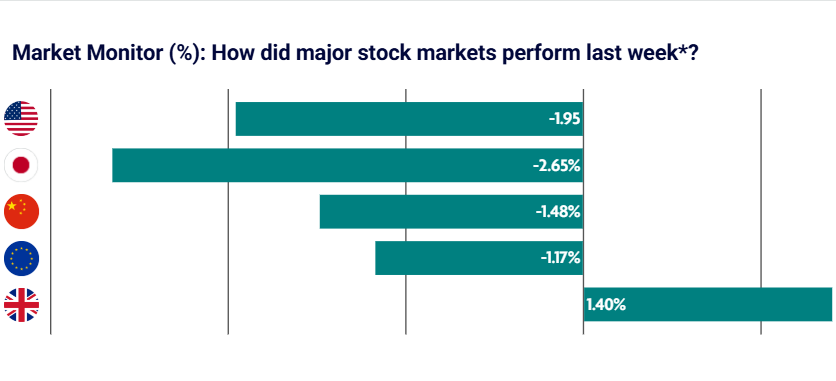

Global equities were broadly weaker, with declines in the US, Japan, Europe and China amid a tech driven sell-off. Meanwhile, the UK market outperformed as investors rotated out into value stocks.

US: Tech sell-off brings equities under pressure

Major U.S. stock indices ended the week mixed, as weakness in large cap technology and AI-related stocks weighed on the Nasdaq Composite and S&P 500, while the Dow Jones Industrial Average and the small-cap Russell 2000 posted gains. Large cap value stocks outperformed growth stocks, and the equal-weighted S&P 500 also surpassed its market capitalisation-weighted counterpart. Inflation data showed price pressures remained elevated but stable, with Personal Consumption Expenditure figures broadly in line with expectations, while personal income and spending rose strongly, highlighting ongoing consumer resilience. Business activity improved modestly in June, supported by both services and manufacturing, although employment softened and supply chain disruptions persisted amid tariffs and geopolitical tensions. First-quarter GDP growth was revised higher to an annualised 2.1% from its prior 1.6% estimate. U.S. real GDP (inflation-adjusted) grew 0.5% in the fourth quarter of 2025.

Japan: Equities under pressure as tech sell-off and profit taking weigh on markets

Japan’s stock markets fell over the week, with the Nikkei 225 down 2.65% and the broader TOPIX index down 2.02%, as early gains in AI-related stocks reversed amid a global technology sell-off and profit taking. The yen weakened towards the JPY 161 level against the U.S. dollar, prompting expectations of possible intervention. Lower oil prices supported Japan by easing inflation pressures and boosting demand for government bonds, with the 10-year JGB yield edging down to 2.60%. Meanwhile, Tokyo’s core inflation rose to 1.6% year-on-year in June, reinforcing expectations of further interest rate rises by the Bank of Japan. In addition, Prime Minister Sanae Takaichi announced a major long-term fiscal plan worth around JPY 370 trillion to boost growth, including investment in AI and semiconductors.

China: Policy support and growth focus takes a backseat to Tech sell-off

China’s equities ended the week lower, with the CSI 300 and Shanghai Composite falling 1.48% and 1.55%, while Hong Kong’s Hang Seng dropped 5.24% amid broader weakness in technology stocks and profit-taking in AI-related shares; the sharper decline in Hong Kong partly reflected its heavier exposure to internet platforms and financials. The People’s Bank of China (PBOC) announced the introduction of a new liquidity tool, including overnight reverse repos, to improve short-term liquidity management, while keeping key loan prime rates unchanged at 3.00% and 3.50% for the 13th consecutive month. Meanwhile, Premier Li Qiang reiterated China’s commitment to innovation-led growth and technological advancement at the Summer Davos forum, reinforcing policymakers’ focus on high-quality growth despite ongoing trade tensions.

Europe: Stocks flat as tech sell off offsets easing inflation expectations

The pan-European STOXX Europe 50 Index ended the week negative, down -1.17% in local currency terms, as an early rally faded following a late-week sell-off in global technology stocks driven by valuation concerns around AI-related shares. Among major markets, Germany’s DAX fell 1.26%, France’s CAC 40 declined 0.43%, and Italy’s FTSE MIB dropped 3.00%. Meanwhile, eurozone inflation expectations eased, with the ECB’s survey showing one-year expectations falling to 3.5% in May, alongside improved growth expectations. Business activity data was mixed, as the flash eurozone composite PMI rose to 49.5, its highest since March, while Germany’s composite PMI slipped to 48, reflecting ongoing economic weakness and uncertainty.

UK: Equities rise despite political uncertainty and weak economic data

The UK was a relative outperformer over the week, with the FTSE 100 rising 1.40% despite broader European markets remaining subdued and a late sell-off in global technology stocks. Investors rotated into value stocks and more defensive sectors, which supported UK equities relative to its regional peers. However, domestic developments highlighted growing economic and political challenges. Prime Minister Keir Starmer announced his resignation after months of pressure, triggering a Labour leadership contest. Meanwhile, economic data pointed to weakening activity, with the Confederation of British Industry (CBI) reporting a sharp fall in retail sales in June as volumes dropped to a weighted balance of -54 amid low consumer confidence and rising prices, while manufacturing conditions also deteriorated, with order books falling to their weakest level since 2020.

What's Important Next: 29 June to 3 July 2026

ECB Central Bank Forum

On Wednesday 1st July, Fed Chair Kevin Warsh, ECB President Christine Lagarde, ECB Vice President Boris Vujcic, ECB Executive Board member Piero Cipollone, ECB Chief Economist Philip Lane, BOE Governor Andrew Bailey and Bank of Canada Governor Tiff Macklem will all be meeting to discuss inflation, growth and monetary policy.

Why it's important

Central bank policy is a key driver of interest rates and the broader economy, so gatherings such as the ECB Forum often generate important headlines and provide opportunities for behind the scenes discussions on the global economic outlook and potential policy coordination (including implications for FX markets such as JPY). Perhaps most importantly, it offers another opportunity to hear the views of the new Federal Reserve Chair, Warsh, particularly on appropriate interest rate levels given current inflation dynamics. Any signals of increased hawkishness could further weigh on US equity markets.

US Employment Data

On Thursday 2nd July, US non-farm payrolls are released, a day earlier than usual due to US markets being closed on Friday for the Independence Day holiday.

Why it's important

Recent labour market data has been relatively robust, allowing the administration to argue that the US economy is performing strongly. However, this release is expected to show moderation, with payroll growth forecast to fall from 172k to around 115k. The idea of a "two-speed" or K-shaped economy remains evident. If these figures reinforce that narrative, attention may return to the extent to which US growth is reliant on a narrow set of sectors, particularly AI and technology. This concentration is a concern for equity markets and highlights that job creation is becoming increasingly uneven, adding to worries that the broader economy is unbalanced.

Comments