Weekly Market Review - 30 March 2026

- Stefan Lubek

- Mar 30

- 4 min read

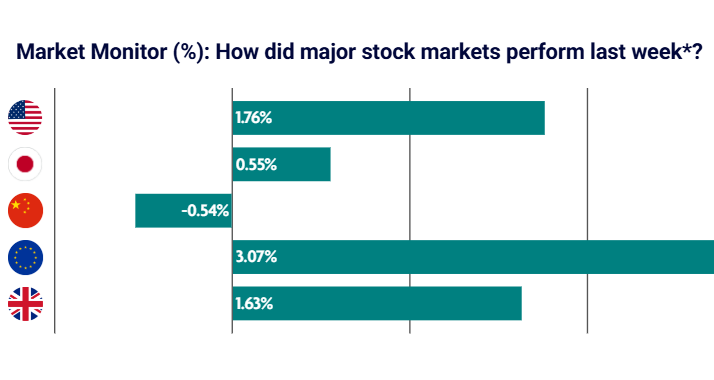

The Middle East conflict and subsequent energy price volatility continued to drive investor sentiment across key global markets. US equities were hit hardest as shifting headlines undermined confidence in a near-term resolution and saw sentiment deteriorate towards the end of the week. UK equities fared best as markets rebounded following last week’s heavy selling.

US: Escalating Middle East conflict weighs on sentiment

U.S. equities finished the week mixed and volatile, driven by Middle East headlines and oil price moves. Early optimism around possible de-escalation faded as conflicting headlines emerged. Small and mid-caps outperformed, snapping four week losing streaks, while the S&P 500, Dow and Nasdaq fell for a fifth week. Large cap value continued to outperform growth. Economic data showed slowing activity and rising inflation pressures. Flash Purchasing Manager Index data (forward-looking economic data) weakened, driven by services, while input costs rose sharply due to energy prices. Jobless claims remained stable, but consumer sentiment fell and near-term inflation expectations jumped. Treasuries were flat overall, though volatility increased as markets priced higher inflation risk. High yield finished broadly unchanged.

Japan: Japanese government releases oil reserves to combat supply risks

Japanese equities were mixed through the week, with the Nikkei 225 index flat and the broader TOPIX index up 1.1%. Rising oil prices weighed on sentiment, given Japan’s reliance on energy imports. The Japanese government released oil reserves and signalled further measures if supply risks increase. The yen hovered near prior intervention levels, keeping foreign exchange risk elevated. Core inflation eased, helped by energy subsidies, but upward pressure from oil prices remains.

China: Investors reassess earnings pressure across energy-sensitive sectors

Chinese equities declined as higher oil prices raised earnings concerns across energy sensitive sectors. Authorities capped domestic fuel price increases to limit inflation pass through. Trade tensions with the U.S. resurfaced as China launched investigations into U.S. trade practices ahead of a potential Xi Trump meeting, although Beijing also signalled a more conciliatory stance earlier in the week. Industrial profits surged early in the year, highlighting an uneven but improving earnings backdrop prior to the Middle East conflict.

Europe: Middle East conflict continues to be key focus for investors

European equities largely flat, as investors assess the likely impact on economic growth from the Middle East conflict. Among major stock indexes, Germany’s DAX was down 0.29%, Italy’s FTSE MIB rose 1.26%, and France’s CAC 40 Index climbed 0.47%. The European Central Bank signalled it remains ready to raise interest rates if inflation pressures persist, though policymakers stressed it is too early to assess the full impact of the Middle East conflict. Eurozone Purchasing Manager Index data softened, new orders contracted, and supply chain disruption increased. German business confidence weakened, despite some improvement in manufacturing. The Organisation for Economic Co-operation and Development (OECD) downgraded its eurozone growth outlook.

UK: The OECD expects the Bank of England to keep interest rates on hold in 2026

UK equities gained 0.49% for the week. Inflation remained unchanged at 3%, although the data pre dates the latest surge in energy prices linked to geopolitical tensions. Growth expectations were downgraded by the OECD, who warned that the UK faces the biggest hit to growth from the Middle East war of all G20 economies. Its 2026 growth forecast was cut to 0.7% from 1.2%, the steepest cut in the OECD’s interim economic outlook. The OECD also highlighted that they expect UK inflation to accelerate to 4% due to higher energy prices. The OECD expects the combination of weaker growth and higher inflation is likely to see the central bank hold off from raising interest rates this year, with interest rate cuts to resume in the first quarter of 2027.

What's Important this week: 30 March to 3 April 2026

Inflation numbers/Consumer Price Index (CPI)

Consumer Price Index (inflation) data from the Eurozone, France, Italy and Japan will be released on Tuesday; and Switzerland on Thursday.

Why it's important

One of the major concerns stemming from the ongoing conflict in the Gulf is the inflationary pass through. Interest rate markets have already begun to price in the risk that central banks may need to raise rates to contain a renewed inflation pulse. As a result, upcoming CPI releases will be closely watched, as they are likely to start reflecting the economic impact of the war.

Any indication that inflation pressures are stronger than expected would increase the strain on policymakers. Unfortunately, the reverse is unlikely to offer much reassurance. Unless there is a meaningful de-escalation in hostilities and a sustained restoration of free passage through the straits, the fear is that the damage already done will persist and entrench higher inflation over the medium term.

USA – Non-Farm Payroll

On Friday, US employment data is released.

Why it's important

With all that is going on, it is easy to forget that the US has a domestic economy and that it is one of the key drivers of global growth. Whilst events in the Gulf are rightly dominating the headlines, it will be useful to have a direct window into the current state of the US economy.

No major surprises or large deviances from trend are expected. However, any sense that the US economy is slower than expected will likely garner an exaggerated market reaction, from already bruised US equity investors. Bottom line, the idea that the AI economic driver might fizzle out a little, and of course the war, are already hurting US equities, and they certainly don't want anything else to worry about. Any positive surprises would quite likely enable, at least in the short term, a bounce in S&P 500 index.

*Source: Bloomberg. All performance measured in local currency.

Issued by Omnis Investments Limited. This update reflects Omnis’ view at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made toensure the accuracy of the information, but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

Comments