Weekly Market Review – 24 November 2025

- Stefan Lubek

- Nov 24, 2025

- 3 min read

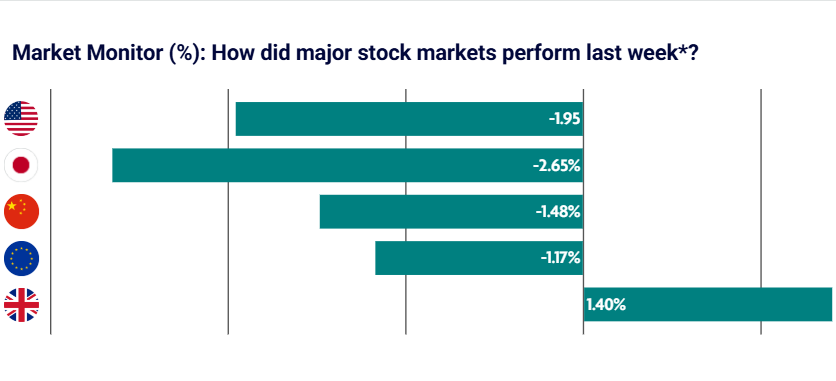

AI-related valuation concerns see global equity markets fall sharply. Chinese equities were pressured the most, while UK equities held up best due to increased expectations of a December interest rate cut.

US: AI valuation concerns outweigh strong corporate earnings and economic data

Despite strong corporate earnings reports and government economic data, U.S. equity markets finished the week lower. Markets were cautious, with investors questioning whether valuations in growth stocks – especially those tied to artificial intelligence – have stretched too far. NVIDIA, the largest company by market capitalisation globally, reported revenue on Wednesday that exceeded analyst forecasts, driven by strong demand for its AI chips. The stock initially rallied, however, sentiment turned negative later in the day, with the stock finishing 3% lower. Meanwhile, the Labour Department’s monthly employment report for September, which was delayed for six weeks by the government shutdown, was finally released on Thursday and provided a somewhat conflicted view of the economy. The report showed that the economy added 119,000 jobs for the month, significantly higher than expected, casting doubt over the likelihood of a December rate cut.

Japan: Equities driven lower by weakness in Japanese AI-related technology stocks

Valuation concerns surrounding AI-related technology stocks saw equities pullback -3.5% in Japan. The new Japanese government approved a JPY 21.3 trillion (US$135bn) economic stimulus package, signalling progress in their expansionary fiscal spending that investors had been expecting. The package comprises spending, tax breaks, and investment targeted at key segments of the economy such as shipbuilding and AI. Consumer inflation remained well above the Bank of Japan’s (BoJ’s) 2% target, with the core consumer price index rising 3.0% year over year in October, in line with expectations and up from 2.9% in September.

China: Stocks fall sharply as AI-related selling intensifies

Mainland Chinese stock markets recorded a weekly loss, mirroring the drop on Wall Street, as investor concerns about frothy valuations in AI-focused names dampened risk appetite. Friday marked the second week of declines for the CSI 300 Index, which rose to its highest level in almost four years earlier in November amid optimism about China’s technology development. No official indicators were released during the week. On the policy front, China’s government is considering new measures to revive the country’s ailing property market amid concerns that further weakness in the sector could destabilise the financial system, Bloomberg reported, citing unnamed officials. Reports of the proposed property measures come as data showed that China’s housing market slump, now in its fourth year, deepened in the third quarter.

Europe: AI valuation concerns and receding expectations of a U.S. interest rate cut weigh on sentiment

Major European stock indices fell for the week. France’s CAC 40 Index dropped 2.29%, Italy’s FTSE MIB declined 3.03%, and Germany’s DAX lost 3.29%. Early readings for the eurozone purchasing managers’ indexes (PMIs) compiled by S&P Global indicated that business activity grew at a solid pace in November. Meanwhile, the latest composite PMI reading indicated that output in Germany continued to expand, albeit at a slower pace than the prior month. Business activity in France’s private sector improved, with strength in services helping to propel overall PMI to 49.9 from 47.7 in the preceding month. Eurozone consumer confidence held steady at an eight-month high according to an estimate from the European Commission.

UK: UK inflation slows seeing expectations of a December interest rate cut increased

UK equities pulled back -1.64% for the week. Annual consumer price inflation in the UK slowed to 3.6% in October from 3.8% in September, as airfare, gas, and utility prices fell, boosting market expectations for another interest rate cut in December. The lowest reading in four months was a tick higher than a consensus estimate in a FactSet poll of economists. Core inflation, which excludes volatile categories like food and energy, fell to 3.4% from 3.5%. Meanwhile, Bank of England (BoE) Chief Economist Huw Pill, who voted to keep interest rates on hold in November, said he did not expect his views on policy to change that much in the short term, according to Reuters. Speaking at a conference, Pill said that wages were still growing significantly above the 2% inflation target. After the BoE’s November policy meeting, Governor Andrew Bailey stated that “further policy easing” is likely to come if disinflation becomes more “clearly established.”

Comments