Weekly Market Review - 20 April 2026

- Stefan Lubek

- Apr 20

- 4 min read

Global equities advanced over the week, supported by signs of de-escalation in the Middle East, strong earnings momentum and generally reassuring economic data. US performed best, while UK equities lagged for the second straight week.

US: Equities rally strongly on de-escalating tensions in the Middle East

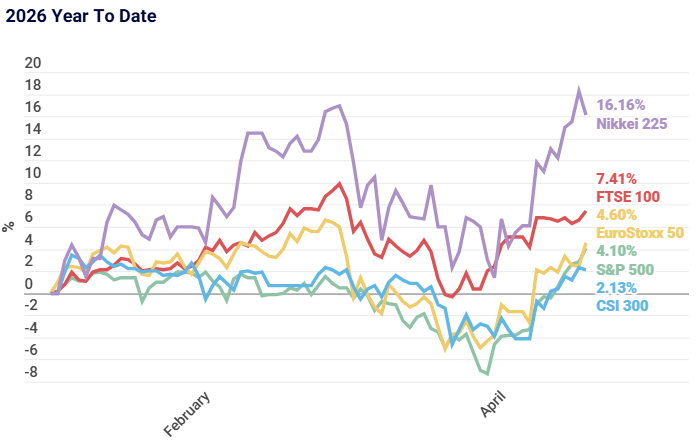

US equities posted a third consecutive week of gains, with several indices reaching record highs. The Nasdaq led performance, rallying +6.84%, driven by continued strength in large cap growth and AI related stocks. Market sentiment improved as ceasefire developments between the US and Iran reduced immediate geopolitical risks, reinforced by confirmation that the Strait of Hormuz was open to commercial shipping. The first wave of first-quarter earnings reports were released by several of the major banks – these were well received as general commentary on economic conditions remained upbeat. Economic data was broadly supportive. Wholesale inflation was cooler than expected, with core producer prices easing further, while jobless claims remained low, pointing to continued labour market resilience. Regional manufacturing surveys improved, suggesting stabilising industrial activity, although housing data remained weak.

Japan: AI optimism, improved corporate governance and solid earnings re-emerge as dominant themes

Japanese equities rose, with the Nikkei 225 index reaching a fresh all-time high. Optimism around AI, improved corporate governance and solid earnings re-emerged as dominant market themes following ceasefire developments. Rate hike expectations for April eased after cautious comments from the Bank of Japan governor, Kazuo Ueda, who highlighted uncertainty stemming from energy price shocks. Business sentiment weakened sharply, reflecting concerns over supply chain disruption linked to Middle East tensions, although bond yields and the yen remained relatively stable.

China: First quarter GDP expands at 5% year-on-year

Chinese equities rebounded modestly after first quarter GDP beat expectations. Growth was supported by exports and industrial output, but underlying momentum remained uneven. Retail sales growth slowed, property investment contracted sharply and fixed asset investment remained subdued. Trade data pointed to weakening external demand, while credit growth undershot expectations despite ample liquidity, suggesting continued softness in domestic demand. Overall, the data reinforced expectations of targeted policy support rather than broad based stimulus.

Europe: The ECB signalled there is no hurry to raise interest rates

European equities rose again, as investors digested corporate earnings and Iran’s announcement that they would reopen the Strait of Hormuz. Germany’s Dax rose 3.77%, Italy’s FTSE MIB rose +2.65% and France’s CAC 40 index rallied 2.0%. The European Central Bank signalled no urgency to raise rates, reinforcing expectations of a prolonged pause in policy tightening. Economic data was mixed. Eurozone industrial production surprised to the upside, but the International Monetary Fund trimmed its growth outlook for 2026, citing ongoing geopolitical risks. German wholesale inflation accelerated sharply due to higher energy and metals costs.

UK: UK equities rise but lag global peers for the second week in a row

UK equities delivered positive returns, but again lagged peers, with large fluctuations in oil majors such as BP and Shell weighing on the index. The lack of big tech exposure also hampered the UK market, given AI stocks rallied globally. From an economic data perspective, the UK economy grew 0.5% month on month in February, which was stronger than expected and reflected an acceleration relative to January. The IMF lowered its 2026 growth forecast for the UK to 0.8%, down from the 1.3% it predicted in January. Of all the G7 economic forecasts, the downward revision to its UK estimate was the largest.

Weekly What's Important Next: Week: 20 April to 24 April 2026

Japanese Inflation

On Friday, we receive Consumer Price Index (CPI) data from Japan.

Why it's important

The Bank of Japan has long operated in a low inflation environment, keeping interest rates close to zero for many years. Over the past year, this has begun to change, with Japanese interest rates moving materially higher. While rates remain low relative to global peers, there is still scope for further increases.

Markets have therefore been watching the Bank of Japan closely for any indication that it may accelerate the pace of tightening, particularly at the short end of the curve. This week, CPI is expected to edge up from 1.3% to 1.4%. Any suggestion that rising inflation is making the Bank more hawkish would likely be seized upon, especially in foreign exchange markets. Last week, the yen broke through key resistance levels, potentially marking the beginning of a correction after a prolonged period of undervaluation.

Deal or No Deal

The US/Iran cease fire ends on Tuesday

Why it's important

Although markets have regained all their losses from the initial outbreak of war, the rhetoric over the weekend has turned markedly more negative. Vice President Vance is travelling to Islamabad once again, while at the same time President Trump has threatened strikes on Iranian bridges and power plants. This matters because the last ships that exited the Gulf before the conflict have now reached their destinations, and no further vessels are currently getting out.

Despite relatively calm market messaging, the reality on the ground is very different. In the US, gasoline spending by small businesses surged in March. In parts of Asia, fuel rationing has already begun. Globally, more airlines are cutting services, while farmers are facing sharply higher fertiliser costs. If the Straits do not reopen soon, shortages of fuel, transportation and agricultural inputs will become increasingly acute, potentially tipping the global economy toward recession. The world needs a deal and fast!

Issued by Omnis Investments Limited. This update reflects Omnis’ view at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information, but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

thapcamtv trực tiếp dạo này mình thấy có người nhắc tới khi nói về các nền tảng giải trí trực tuyến nên cũng thử mở vào xem cách họ bố trí giao diện ra sao. Mình không đi sâu vào nội dung hay từng trò cụ thể, mà chủ yếu quan sát cách các chuyên mục được phân chia trên trang và cách thông tin hiển thị cho người dùng. Nhìn tổng thể thì các khu như thể thao, casino, game bài hay slot thường được sắp xếp theo từng nhóm khá rõ, hiển thị dạng khối và danh sách nên lướt qua cũng dễ theo dõi. Các bảng dữ liệu được trình bày dạng cột khá gọn, giúp quan…

hit club mình thấy dạo này nhiều người nhắc nên cũng ghé thử cho biết, kiểu vào xem giao diện với cách họ trình bày thôi chứ chưa chơi gì. Ấn tượng đầu là trang nhìn sáng sủa, chữ không bị dày đặc, mấy khối nội dung chia ra rõ nên lướt khá nhanh. Mình có để ý họ nhấn mạnh vụ bảo mật SSL 256-bit ngay phần giới thiệu, đặt chỗ dễ thấy nên đọc cái là hiểu họ muốn nói gì. Menu cũng gọn, bấm qua lại giữa các mục không bị rối hay phải mò lâu. Nói chung cảm giác dùng trên web khá mượt, nhất là mấy tiêu đề chia section nhìn phát là định hướng…

luongson tv mình vừa lướt thử cho biết vì thấy bạn bè nhắc nhẹ, chủ yếu xem giao diện có dễ dùng không thôi. Vào trang cái là thấy bố cục khá thoáng, mấy khối nội dung chia ra rõ nên kéo xuống không bị rối mắt. Mình để ý cái menu đặt ngay chỗ dễ nhìn, bấm chuyển qua lại mấy mục nhanh, không phải mò lâu. Chữ với khoảng cách dòng nhìn ổn, kiểu liếc qua là nắm được ý chính chứ không bị dồn chữ sát nhau. Mình không ngồi đọc kỹ nội dung, nhưng cảm giác thao tác khá mượt, không bị “lạc” trong trang. Nói chung nhìn thân thiện, đơn giản vừa đủ, đặc biệt…