May 2026 market update - Markets rebound but energy risks linger

- Stefan Lubek

- May 7

- 4 min read

Updated: May 15

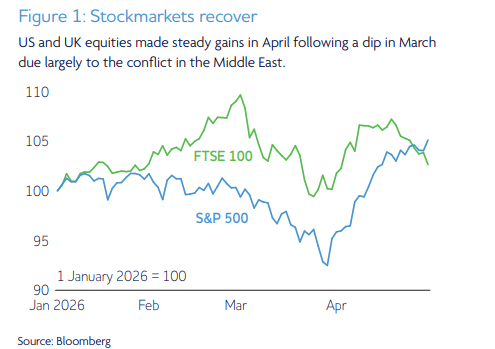

Global markets rallied in April, but the Iran conflict and surging oil prices continue to cloud the outlook.

Markets recover as tensions persist.

Global markets recovered in April, with stocks rebounding from March’s losses. US equities climbed to fresh highs, supported by strong earnings and AI-driven growth, while the FTSE 100 regained ground. European and Asian markets also moved higher.

Central banks are facing a more complex backdrop as the US–Iran war adds to inflationary pressures and uncertainty around growth. Optimism briefly improved following a two-week ceasefire, but negotiations have since stalled.

Disruption in the Strait of Hormuz has persisted, keeping oil prices volatile. Crude rose above $126 a barrel at one point, the highest since 2022, after President Donald Trump warned the US blockade of Iranian ports could last for months.

Fed keeps rates on hold.

The US Federal Reserve (Fed) held interest rates for a third consecutive meeting as inflation rose and uncertainty increased. US inflation jumped from 2.4% in February to 3.3% in March, driven largely by higher energy prices.

The increase is the largest in nearly two years, echoing the inflation shock seen after the invasion of Ukraine. Consumer sentiment has fallen to a record low as households react to rising costs. Gasoline prices have climbed above $4 a gallon, raising concerns about weaker consumer spending.

Despite this, the labour market remained resilient. Employers added 178,000 jobs in March, while unemployment edged down to 4.3%.

UK inflation rises.

The Bank of England held interest rates at 3.75% in April despite rising price pressures. UK inflation increased to 3.3% in the year to March, up from 3% the previous month, driven largely by higher fuel costs.

Rising prices and economic uncertainty have pushed consumer confidence to a two-year low. The UK’s reliance on imported gas leaves it exposed to energy shocks, with inflation expected to remain elevated over the short to medium term.

The labour market showed mixed signals. Unemployment fell to 4.9%, while regular pay growth slowed to 3.6%, which is its weakest level since late 2020.

China’s growth rebounds.

China’s economy grew 5% year-onyear in the first quarter, showing resilience despite disruption from the Iran conflict. Industrial output rose 5.7% in March and retail sales increased 1.7%.

The economy has so far absorbed the shock, supported by large oil reserves and renewable energy. But growth is expected to slow later in 2026, with inflation beginning to rise as energy costs feed through.

In Europe, the European Central Bank (ECB) kept rates on hold at 2% for a third meeting. Eurozone inflation rose sharply to 2.6% in March from 1.9% in February, driven by higher energy prices.

Private sector output weakened, with activity slipping and demand softening. Manufacturing held up better, but falling confidence and rising costs have increased concerns about stagflation.

Market-moving events

Middle East tensions persist. A ceasefire is in place, but the Strait of Hormuz remains closed, keeping upward pressures on the prices of oil, gas and key raw materials used in fertiliser, metals and semiconductor production. These supply constraints are likely to persist and could continue to influence markets in the months ahead.

Central banks hold steady. Economic data was mixed and uncertainty remains high. Major central banks left rates unchanged while highlighting inflation risks. The Bank of England outlined scenarios suggesting further rate hikes this year, followed by cuts later in the cycle, underscoring the difficult policy trade-off.

Equities diverge. Despite elevated oil prices, equities rallied over the month, led by the US as earnings came into focus. Mega-cap technology results beat expectations, though market reactions were mixed, with Meta in particular falling after raising capital expenditure guidance

Increased short-dated bonds. During the month, we reduced exposure to both UK and European equities, removing our tactical overweight in both regions. We added exposure to short-dated bonds as a further defensive tilt, with a view to protecting investor capital from any future equity market volatility. In agility, proceeds were reallocated to short-dated Japanese government bonds, reflecting more attractive valuations and aiming to benefit from a strengthening Japanese yen.

Tactical positioning detracted over the month. Our underweight exposure to global equities, particularly the US market, had a negative impact relative to the Strategic Asset Allocation. Markets rallied strongly as investors priced in a short conflict in the Middle East and continued resilience in corporate earnings.

Remain cautiously positioned. Portfolios remain modestly underweight equities, with a particular focus on US equities, and overweight bonds. This reflects ongoing concerns around elevated equity valuations and the risk that any escalation in the Middle East could begin to weigh on economic growth.

Issued by Omnis Investments, which is authorised and regulated by the Financial Conduct Authority. Registered address: Auckland House, Lydiard Fields, Swindon SN5 8UB. This update reflects our view at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis Investments is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance

https://keonhacai5.net/ dạo này thấy mọi người nhắc hoài nên mình cũng bấm vào nghía thử cho biết. Mình không đọc sâu đâu, chủ yếu xem giao diện với cách họ sắp xếp nội dung có dễ nhìn không. Vừa vào là thấy bố cục khá gọn, kiểu chia thành từng khối rõ ràng nên lướt xuống không bị rối mắt. Mấy phần thông tin họ để theo dạng bảng/cột nhìn cái là hiểu nhanh, đỡ phải kéo qua kéo lại tìm từng dòng. Menu đặt ngay chỗ dễ thấy nên mình chuyển qua vài mục thử cũng tiện, không bị cảm giác “lạc” trong trang. Nói chung trải nghiệm lướt ổn vì các khối nội dung và bảng cột trên…

sun win mình vừa lướt thử vài phút vì thấy bạn bè nhắc hoài, kiểu vào xem giao diện là chính. Cảm giác đầu tiên là trang làm khá gọn, chia nội dung theo từng khối nên nhìn phát hiểu ngay, không bị ngợp chữ. Mình thấy cái tiêu đề kiểu “cổng game chính thức 2026” để khá nổi, nên cũng yên tâm là đang ở đúng trang chứ không phải mấy trang linh tinh. Lướt trên điện thoại ổn, chữ dễ đọc, kéo xuống không bị giật lag gì. Mình không có thử sâu game, chỉ để ý cách họ sắp xếp thông tin thôi, nhìn hiện đại hơn mình tưởng. Nói chung phần bố cục và các khối…

rophim hôm trước thấy mọi người share nhiều quá nên mình ghé thử cho biết. Vào cái là trang hiện nội dung khá nhanh, không bị mấy lớp hiệu ứng che màn hình hay bắt chờ lâu nên cảm giác “nhẹ” hẳn. Mình chủ yếu lướt xem giao diện thôi chứ chưa kịp chọn phim kỹ, nhưng thấy cách họ bày phim theo từng khối nhìn gọn, kéo xuống một phát là thấy thêm nhiều mục. Thử mở trên điện thoại cũng ổn, bấm qua lại không bị loạn hay khó tìm nút. Có cái mình thích là phần phim HD vietsub nhìn rõ ràng, không phải mò trong đống chữ nhỏ. Nói chung nhìn qua đã thấy bố cục…

https://soicau247.com/ dạo này mình thấy mấy đứa bạn hay nhắc nên mình ghé thử cho biết. Không phải kiểu vào để “chốt số” gì đâu, mình chỉ xem trang họ trình bày ra sao thôi. Cảm giác đầu tiên là bố cục khá dễ nhìn, thông tin chia theo từng mảng nên kéo xuống không bị ngợp. Mình thích nhất đoạn “Xổ số Miền Bắc ngày 03/06/2026” vì nó để dạng bảng đầu/đuôi lô tô, nhìn một phát là hiểu đang tra gì. Mấy tiêu đề theo ngày cũng đặt rõ ràng nên bấm qua lại không bị lạc. Nói chung lướt nhanh vẫn nắm được nội dung chính, đặc biệt là cái bảng đầu/đuôi lô tô trình bày gọn…