March Market Update - Markets rise amid easing tariff fears

- Stefan Lubek

- Mar 2

- 4 min read

Updated: Mar 18

*NB: This update was prepared at the end of February 2026, before the US and Israeli attacks on Iran.

Markets steady as tariff fears ease.

Global market concerns surrounding tariffs eased when the Supreme Court ruled that the mechanism used in President Trump’s sweeping Liberation Day tariffs were unlawful. Trump subsequently announced new tariffs would come into effect at 15% (via another mechanism). In the end a 10% blanket rate was added. Whilst the administration can still table new tariff measures, the court ruling suggested that the raising of revenue squarely sits with Congress, so will need its approval moving forward. Markets reacted positively as it largely ruled out a repeat of Liberation day and makes tariff policy more procedural.

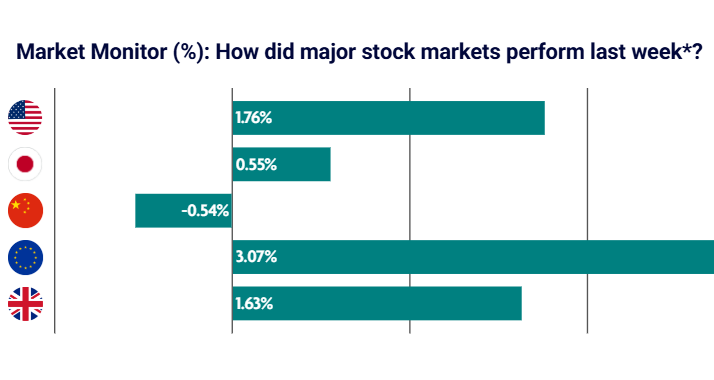

US stocks recovered after worries about the impact of artificial intelligence on company profits proved short-lived. Even so, market leadership has broadened, with investors rotating away from the US and into other regions year to date (figure 1). After a strong start to 2026, European equities climbed to record highs following a string of upbeat company results. Japanese stocks also broke records after Prime Minister Sanae Takaichi secured a decisive election victory, clearing the way for increased spending and tax cuts.

US inflation eased more than expected in January to 2.4%, down from 2.7% the previous month, strengthening the case for the US Federal Reserve (Fed) to cut rates later in the year. The labour market also showed signs of improvement, with employers adding 130,000 jobs and unemployment falling to 4.3%. However, overall growth remained subdued at 1.4% in the fourth quarter, partly reflecting the impact of the longest federal shutdown in history.

UK gains momentum.

The FTSE 100 climbed above 10,000 for the first time, supported by strong corporate earnings and softer inflation. The pound also rose to a four-year high against the dollar. Britain’s economy grew by 0.3% in November, its fastest pace since June, driven by a rebound in manufacturing and services activity.

Inflation fell significantly to 3% in January from 3.4%, its lowest level since March last year, increasing expectations of a Bank of England rate cut in March. Although the Bank kept interest rates on hold at 3.75% at the start of February, it signalled that cuts are likely later in the year as inflation moves back towards its 2% target. Signs of labour-market weakness persist, with unemployment near a five-year high and wage growth continuing to ease.

Europe and Asia mixed.

The European Central Bank (ECB) left interest rates unchanged at 2% after eurozone inflation slowed to 1.7% in January, below its target for the first time since May. Despite geopolitical tensions and trade uncertainty, the eurozone economy expanded by 0.3% in the final quarter, unchanged from the previous three months. Business surveys suggest a gradual recovery is underway, led by Germany, with confidence rising to a 20-month high.

China continues to face headwinds. While the economy grew 5% last year, meeting its official target, domestic demand remains weak. Consumer inflation slowed to 0.2% in January and producer prices remained in deflation, highlighting persistent price pressures. Although China reported a record $1.2 trillion trade surplus in 2025, driven by strong exports to non-US markets, fourth-quarter growth slowed.

Figure 1: Leadership shifts

Regional stock markets have outperformed so far this year as investors rotate beyond

Market-moving events

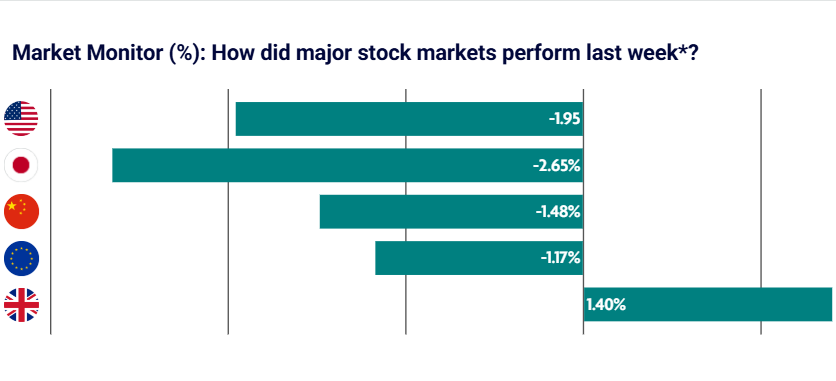

Rotation broadens. The Dow Jones Index passed the 50,000 milestone in early February, reaching a new intraday high, while the S&P 500 moved largely sideways. At the same time, Microsoft fell sharply from late January levels, highlighting a clear rotation away from technology and into broader US sectors. We expect this shift away from tech to continue as investors reassess whether AI capital spending can translate into sustainable earnings growth.

Diversification gathers pace. Diversification beyond the US accelerated, with strong overseas performance. Korea’s market rose 27% to a record high on expectations it will benefit from AI investment. The FTSE 100 and France’s CAC 40 index also reached new highs, while Japan extended its strong run, supported by international inflows into government bonds.

China under pressure. China continues to face economic headwinds. While growth remains around 5%, data points to slowing momentum. Manufacturing PMI slipped into contraction at 49.3, and half of China’s regions lowered their 2026 growth targets. Although less severe than previous downturns, this signals a cautious outlook. A more realistic approach from Beijing could allow fiscal resources to be deployed more effectively and support stabilisation.

Tactical positioning rewarded. Our tactical positioning benefited from a rotation out of US

technology, which created a drag on the S&P 500. US energy and US small caps subsequently outperformed the index, driving positive TAA performance.

No changes made during the month. Following January’s trades out of US large caps and intoUS small caps, and a portfolio rebalance, we left the portfolio unchanged in February.

Remain cautiously positioned. We retain a moderate overweight position in bonds and an

underweight allocation to equities, particularly US large companies. We continue to expect a broadening of the equity market rally away from US large caps, as we believe the AI narrative is likely to come under greater scrutiny.

Issued by Omnis Investments, which is authorised and regulated by the Financial Conduct Authority. This update reflects our view at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis Investments is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

Approved by Omnis Investments on 1 March 2026

Comments