Weekly Market Review – 17 November 2025

- Stefan Lubek

- Nov 17, 2025

- 3 min read

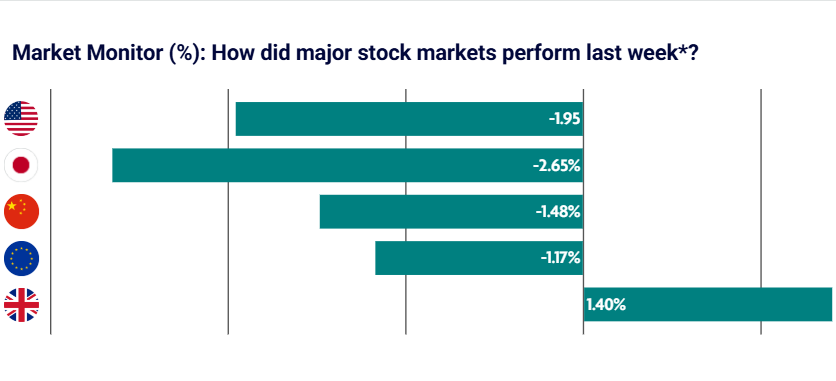

A largely muted week for global equities, despite a significant number of headlines. Investor sentiment was broadly supported by the end of the US government shutdown, however, economic growth concerns and valuation concerns in the artificial intelligence space provided something for both the bulls and the bears. European equities were the standout performer, while Chinese equities lagged.

US: Hawkish commentary from Federal Reserve officials and valuation concerns see AI stocks selloff

U.S. equity markets ended the week with mixed results. The S&P 500 was largely flat, while the Nasdaq, S&P MidCap 400, and Russell 2000 pulled back. The week was marked by a rotation out of high-growth tech stocks, especially those tied to artificial intelligence, as investors grew concerned surrounding lofty valuations and potential regulatory scrutiny. The longest U.S. government shutdown on record ended on Wednesday evening after President Donald Trump signed a spending bill that will keep the government funded through to 30 January 2026. Atlanta Federal Reserve President Raphael Bostic outlined concerns over ambiguous labour market data, highlighting we are unlikely to see aggressive rate cuts amid persistent inflation. Two other Federal Reserve officials echoed similar caution, which saw the chance of a December rate cut fall to 46%, down from 95% a month ago.

Japan: Equities rise slightly on improving investor sentiment

Japanese equities rose slightly for the week, as global sentiment was supported by the U.S. ending the country’s longest government shutdown in history. Conversely, continued concerns about overstretched valuations of companies with revenue streams linked to artificial intelligence weighed on Japan’s technology sector. Meanwhile, expectations of more loose fiscal policy and caution surrounding further interest rate rises under new Prime Minister Sanae Taikachi pressured the yen. She shared her concept that responsible, yet aggressive, fiscal spending is required to boost economic growth.

China: Stocks pullback from record high on slowing growth concerns

Mainland Chinese stock markets retreated as investors pocketed gains a week after the leading domestic benchmark rose to its highest level in almost four years. The latest batch of official indicators showed that China’s economy lost steam as it entered the fourth quarter. Fixed asset investment shrank 1.7% in the first 10 months of the year, a record drop for the period, according to China’s statistics bureau. Industrial production rose a weaker-than-expected 4.9% in October from a year ago, while retail sales rose 2.9%, the fifth straight month of slower growth.

Europe: Equities rise on end of U.S. government shutdown

Most major European stock indices rose for the month. Germany’s DAX tacked on 1.30%, France’s CAC 40 Index advanced 2.77%, and Italy’s FTSE MIB climbed 2.51%. This was despite eurozone industrial output being weaker than expected. However, gains were dampened by concerns surrounding the artificial intelligence space. Investor sentiment fell in Germany, according to the ZEW institute. Investors remain concerned that the government’s defence and infrastructure spending may be insufficient to revitalise their economy.

UK: UK equities deliver modest gains as soft economic data dents investor enthusiasm

UK equities were broadly flat, as weaker-than-expected UK labour market data and economic growth data dented investor risk appetite. Unemployment in the three months through September increased to 5% for the first time since January 2021. Wage growth also slowed in the third quarter, with the annual growth rate in weekly earnings, excluding bonuses, easing to 4.6% from 4.8% in the prior period. Gross domestic product (GDP) growth slowed to 0.1% in the third quarter, which was below consensus estimates of 0.2%. These data points saw investors sharply increase their bets on the Bank of England cutting interest rates in December.

Comments