Weekly Market Review - 12 January 2026

- Stefan Lubek

- Jan 12

- 3 min read

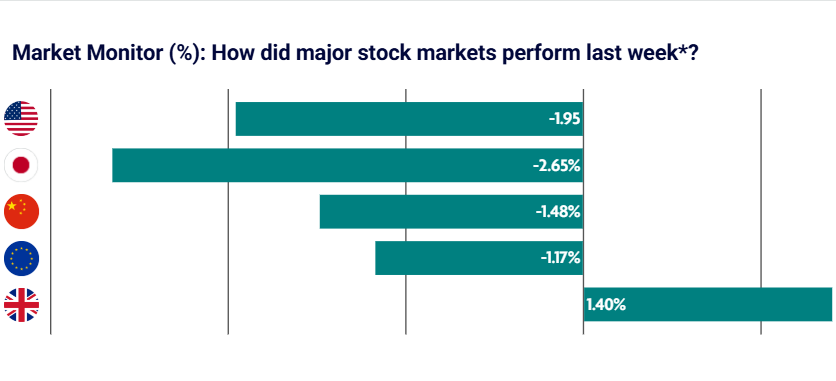

Global equities rallied in the first full week of trading for 2026, as investors looked through rising geopolitical tensions. Japanese equities led the charge, while we saw a broadening of the market rally in the United States

US: EQUITIES RALLY AS INVESTORS LOOK PAST MOUNTING GEOPOLITICAL TENSIONS

Small cap and value stocks outperformed large cap growth shares, which have dominated returns in recent years. Aerospace and defence companies initially sold off following comments from Trump that they would be barred from paying dividends or repurchasing shares unless they accelerated military hardware production, but defence stocks rebounded the next day after the administration proposed a sizable increase in military spending. Labour market data surprised to the downside with job growth moderating in December and prior months’ figures revised lower, while the unemployment rate ticked down to 4.4 percent from a revised 4.5 percent in November. Institute for Supply Management (ISM) data showed US manufacturing activity contracted for the tenth consecutive month in December, with Manufacturing PMI data falling to 47.9, the lowest reading of 2025. Meanwhile, services activity expanded for the tenth straight month with gains in new orders, business activity, and a rebound in employment pushing the Services PMI to its highest level of the year.

JAPAN: EQUITIES RALLY ON GOVERNMENT STIMULUS HOPES

Japanese equities registered strong gains over the week, as geopolitical tensions between China and Japan failed to dent the markets’ advance. Technology companies continued to rally while yen weakness provided a boost to export-oriented companies and trading houses. The Japanese yen depreciated as investors became concerned over the government’s massive spending plans to stimulate economic growth. Bank of Japan Governor Kazuo Ueda stated that the central bank will keep raising rates in line with improvements in the economy and inflation. He added that the mechanism between moderate wage growth and inflation is likely to be maintained.

CHINA: DOMESTIC TECH OPTIMISM DRIVES CHINESE EQUITIES TO 4-YEAR HIGHS

Chinese equities rallied to a 4-year high throughout the week, fuelled by artificial intelligence trades. Outstanding loans taken out by investors to buy stocks neared a record according to Bloomberg. On the economics front, inflation data showed that consumer price growth picked up in December, though producer prices fell for the 39th straight month. China’s consumer price index (CPI) rose 0.8% in December from a year ago, in line with forecasts, the country’s statistics bureau reported. The producer price index fell 1.9%, the smallest decrease in more than a year.

EUROPE: STOCKS RALLY ON OPTIMISM AROUND ECONOMIC OUTLOOK

Major indices rose for the week, with Germany’s DAX rallying 2.94%, France’s CAC 40 Index gaining 2.04%, and Italy’s FTSE MIB adding 0.76%. The eurozone economy appeared to be strengthening toward the end of 2025, amid evidence that Germany may have turned a corner. Industrial production in Germany, France, and Spain came in better than forecast in November, with German output increasing sequentially by a seasonally adjusted 0.8% rather than shrinking 0.5% as predicted by consensus estimates. Headline annual inflation in the eurozone slowed to the European Central Bank’s target of 2.0% in December, down slightly from November. Tomasz Wieladek, chief European macro strategist at T. Rowe Price, noted that services inflation remains stronger and more persistent than is consistent with the ECB’s target, which he believes will continue to worry policymakers.

UK: EQUITIES RALLY ON EXPECTATIONS FOR FURTHER INTEREST RATE CUTS IN 2026

UK equities rallied on the back of hopes for 2 further interest rate cuts in 2026. The UK 10-year bond yield posted its biggest fall since April, which saw equities well supported. Talks of a mega-merger between Rio Tinto and Glencore also buoyed UK equities, as resources rallied. Separately, the number of mortgages approved by British lenders for house purchases fell to 64,530 in November from 65,010 in October, Bank of England data showed. Halifax, a mortgage lender, said house prices unexpectedly fell in December by 0.6% sequentially, after dipping 0.1% in November, as economic and tax uncertainty dampened sentiment at the end of last year.

*Source: Bloomberg. All performance measured in local currency.

Issued by Omnis Investments Limited. This update reflects Omnis’ view at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information, but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

Comments