September market update - Global stock markets rally to record levels

- Stefan Lubek

- Sep 5, 2025

- 4 min read

Updated: Sep 11, 2025

Hopes of lower US interest rates and strong company earnings results drive share prices higher

Record highs.

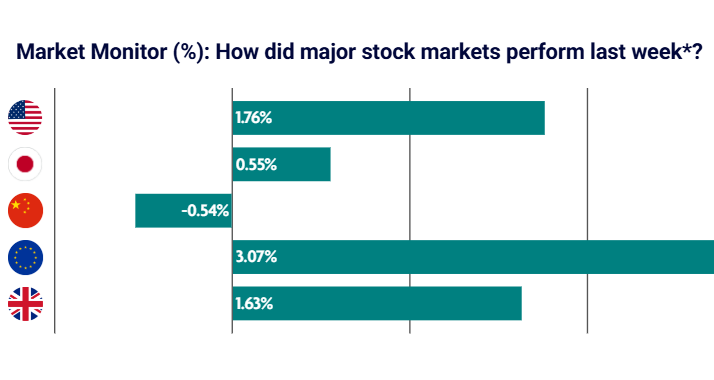

Global stocks hit record levels after steady US inflation strengthened expectations of a Federal Reserve (Fed) rate cut in September, while an extension of the US–China trade truce boosted sentiment. Earnings season added further momentum, with most companies beating forecasts. However, UK government borrowing costs climbed as yields on long-term bonds increased.

US consumer price inflation held steady at 2.7% in July. Core inflation, excluding food and energy, rose to 3.1% – the fastest pace in six months. US producer prices, a measure of wholesale costs, increased 3.3% year-on-year, another sign tariffs are weighing on the economy.

Fed Chair Jerome Powell signalled a possible September cut, while suggesting the inflationary impact of President Donald Trump’s tariffs may be temporary. Tensions escalated after Trump ordered the removal of governor Lisa Cook, giving him the chance to nominate a replacement and increase his influence.

The jobs market has become a key focus for the Fed. Payrolls for May and June were revised lower, followed by a weak July report. Unemployment also rose to 4.2% from 4.1%. This softer trend has been central in shifting expectations towards a September rate cut.

UK inflation surprise

UK consumer prices rose after summer travel pushed air fares higher. The annual rate rose to 3.8% in July, up from 3.6% the previous month and the highest in 18 months. The Bank of England cut rates for the fifth time in a year, lowering them by 0.25 percentage points to 4%, while warning that food prices could add further pressure.

The move brings borrowing costs to their lowest since March 2023, against a backdrop of slowing growth. Most economists expect Chancellor Rachel Reeves will have to raise taxes in the Autumn Budget, as subdued growth and higher borrowing costs have made it harder to meet fiscal targets.

Growth slowed to 0.3% in the second quarter, down from 0.7% in the first. The labour market also cooled: unemployment rose to a four year high of 4.7% in the three months to June, while vacancies fell.

Asia rallies on tariff pause.

Asian equities advanced after Trump signed an executive order pausing higher tariffs on Chinese imports for 90 days. China’s economy weakened in July as domestic and external pressures weighed. Industrial output grew 5.7%, down from June’s 6.8%, while retail sales rose at the slowest pace since December 2024.

Exports were a relative bright spot, climbing 7.2% year-on-year, while imports grew at the fastest pace in a year as businesses moved quickly to benefit from the pause. Despite the truce preventing sharper tariff hikes, manufacturers remain under pressure from weak demand and falling factory prices. Even so, Chinese equities rallied strongly, with the mainland CSI 300 index gaining 10% over the month (figure 1).

Meanwhile, eurozone inflation stayed at 2% in July, with lower energy prices and a stronger euro keeping costs contained. GDP rose just 0.1% in the second quarter, compared with 0.6% in the first, though demand has held up.

Trade tensions with the US eased after an agreement to apply 15% tariffs on most exports, averting a broader trade war between two of the world’s largest economies.

Market-moving events

Tariff challenges mount. A US court ruled Trump’s use of emergency powers to impose trade tariffs unlawful, though most remain in place pending appeal. The decision may change how tariffs are applied rather than the policy itself. The US also added a 25% tariff on Indian goods after talks over agriculture stalled.

BoE signals caution. The Bank of England cut rates by 0.25% to 4% in August, with a closer vote than expected. Inflation is now forecast to peak at 4%, led by food and energy. Another cut this year looks less likely, though markets still see gradual easing into 2026.

US jobs weakness emerges. Revised data showed job growth below the level needed to keep unemployment steady, with large downward revisions unusual outside recessions. At Jackson Hole, Fed Chair Jerome Powell said the “shifting balance of risks” could warrant a September cut. Even so, high inflation suggests any easing will be gradual.

Investment highlights

Portfolio rebalance with new positioning. In June, we rebalanced portfolios and increased

exposure to two existing funds, reflecting our latest tactical views. These changes align the

portfolios with emerging global market opportunities.

European allocation increases. We added to the Omnis European Equity Leaders Fund

and trimmed exposure to the Omnis Asia Pacific (ex-Japan) Equity Fund following strong

performance. With interest rates expected to fall and governments planning more spending, we see a supportive backdrop for European equities. Extra commitments from Germany, alongside wider European stimulus efforts, should also help.

Focus on US smaller companies. We increased our position in the Omnis US Smaller Companies Fund and reduced exposure to the Omnis US Equity Leaders Fund. Smaller companies now offer a stronger earnings growth outlook than larger peers and, at current valuations, present a more attractive risk-reward opportunity. We expect this to drive small-cap outperformance in 2025.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

The balance between strong earnings and mounting tariff pressures shows just how finely markets are being influenced by both corporate resilience and political decisions. Interesting to see small-cap opportunities emerging in the US—often overlooked compared to the mega-caps, but potentially a strong driver of returns as the cycle evolves.