November market update - Global Equities Rally on Trade Deal Optimism

- Stefan Lubek

- Nov 7, 2025

- 4 min read

Easing trade tensions and upbeat company earnings results lifted global markets in October

Strong start to earnings season

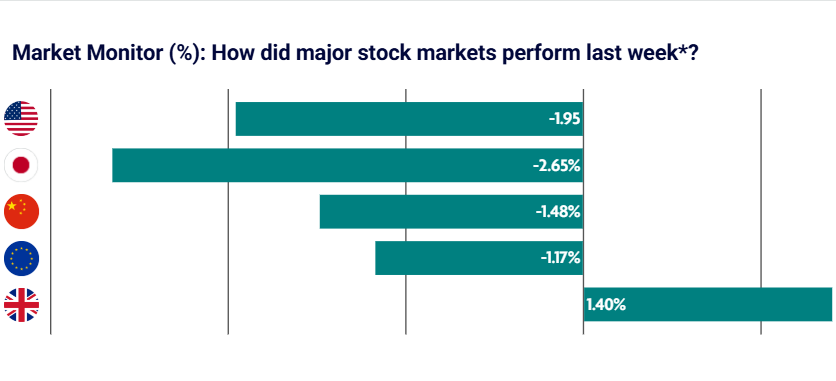

Global stock markets rallied in October, buoyed by optimism around corporate earnings and easing trade tensions between the US and China. It was another strong month for US equities after softer-than-expected inflation figures boosted hopes of further rate cuts.

Earnings season has got off to a good start, with around 85% of S&P 500 companies beating expectations so far – the highest in four years. The Federal Reserve (Fed) lowered rates for the second time this year by a quarter percentage point to support the slowing job market. It is the first time the Fed’s rate-setting committee has cut rates without access to the official jobs report since it was established in the 1930s, due to the ongoing government shutdown.

Republicans and Democrats remain deadlocked over a federal budget, making this the longest full government shutdown in US history. The shutdown has blacked out crucial economic data – from jobs to overall growth – complicating the Fed’s decision-making. Inflation data is also unlikely to be released in November.

UK inflation holds

UK inflation unexpectedly held steady at 3.8% in September for the third month in a row. Following a recent resurgence driven by higher food prices and the increase in National Insurance, economists believe inflation may now have peaked.

The UK job market continues to show signs of weakening, with pay growth slowing and unemployment rising. Unemployment rose to 4.8% in the three months to August, up from 4.7% in July. Meanwhile, annual wage growth in the same period eased slightly to 4.7% from 4.8%. All eyes are now on the upcoming UK Budget, with Chancellor Rachel Reeves expected to raise taxes and cut spending.

US - China reach deal on tariffs

The US and China have reached a preliminary trade deal, lowering US tariffs in exchange for access to China’s rare earth minerals. President Donald Trump said the one-year agreement will reduce US tariffs on Chinese goods from 57% to 47%. The US relies heavily on rare earth metals for advanced technologies, including cars, aircraft and weapons.

China’s exports to the US fell 27% in September compared with a year earlier, even as overall global exports hit a six-month high. Meanwhile, China’s total exports rose 8.3% year-on-year in September, up from 4.4% in August. However, its manufacturing sector contracted for a sixth consecutive month.

Japan’s stock market surged to a record high after the country’s parliament elected Sanae Takaichi as the country’s first female prime minister. Her incoming administration is expected to consider an increase in higher defence spending, tax cuts and a revival of Japan’s suspended nuclear power plants.

Meanwhile, there was further political turmoil in France after new Prime Minister Sébastien Lecornu unexpectedly resigned before being reappointed. Eurozone inflation had risen to 2.2% in September – the first time it has exceeded the European Central Bank’s (ECB) 2% target since April – but then dipped to 2.1% in October. Private sector activity also logged its strongest growth in almost two years, offering a glimmer of optimism for the eurozone economy.

Market-moving events

Keep calm and carry on. The global stock market rally continued despite renewed talk of an artificial intelligence (AI) bubble. Once again, the US tech sector led the charge, even amid concerns about stretched valuations. Amazon’s share price jumped 11% after third-quarter earnings beat expectations, while Nvidia gained around 8%.

Economic data remains resilient. Purchasing Managers’ Index (PMI) data from around the world largely stayed above 50, signalling ongoing growth. In developed markets, inflation appears to be under control, giving central banks room to take a more accommodative stance. The US Federal Reserve cut interest rates by a quarter percentage point for the second time this year

First signs of cracks? Tariff negotiations continue to make progress, with the US dollar supported by positive signals from US–China talks. The main concern has been rising unease over potential credit defaults, following J.P. Morgan CEO Jamie Dimon's warning about "cockroaches" appearing in the financial system. The bankruptcy of US car parts manufacturer First Brands, with debts of $10–50 billion, is notable but, for now, defaults remain limited.

Investment highlights

No changes in October. The investment team are actively monitoring portfolio positioning and are anticipating making some additional changes before the end of the year.

Risk appetite was again rewarded. Global equities performed strongly, with broad risk sentiment assisted by continued AI investment, strong third-quarter company earnings, easing monetary policy and resilient economic growth.

Remain cautiously positioned. We have a slight overweight in bonds and underweight in equities. We remain underweight the US due to a combination of high valuations and increased concentration risk. Our base case expectation of falling inflation, easing monetary policy and a soft-landing remains, although risks of a deeper recession remain elevated.

This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance

Comments