May market update - Markets recover despite ongoing tariff turmoil

- Stefan Lubek

- May 6, 2025

- 4 min read

Updated: Sep 11, 2025

Investor sentiment improves after early-April volatility sparked by US policy shifts

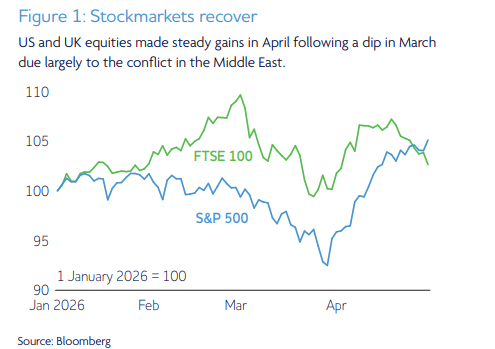

Markets Stumble, then steady

After falling as much as 12% in early April, global equity markets rebounded to finish the month where they began.

Policy signals calm markets.

Global markets regained ground after a shaky start to the month, as concerns over the impact of US tariffs began to ease. Markets were initially rattled by uncertainty surrounding President Donald Trump’s trade measures, but sentiment improved after Washington signalled a softer stance.

Bond markets were also volatile, with US Treasury yields surging (which means bond prices fell) on fears about the economic fallout. Confidence returned after Trump announced a 90-day pause on higher tariffs for most countries, although levies on China still rose by 145%. The US dollar slid to a three-year low after Trump intensified criticism of Jerome Powell, the chairman of the US central bank, the Federal Reserve.

The US economy shrank by 0.3% in the first quarter of 2025, largely due to companies rushing to import goods ahead of the tariffs. This compared with a 2.4% growth in the economy in the previous quarter. US inflation fell by more than expected in March, dropping to 2.4% from 2.8%, though economists warn prices could rise again as imports become more expensive.

Meanwhile, the labour market remains solid, despite federal workforce cuts. But falling consumer confidence and weakening indicators are fuelling fears of a sharper slowdown. The broad scope of the tariffs is adding to uncertainty, with growing concern the US economy could tip into recession.

UK economy surprises with modest growth.

The UK economy grew by 0.5% in February, exceeding expectations and offering a boost for Chancellor Rachel Reeves. Still, escalating trade tensions and domestic headwinds mean the outlook remains fragile.

UK inflation eased to 2.6% in March from 2.8%, offering a glimmer of relief for households and businesses. With risks to economic growth mounting, markets now expect the Bank of England to cut interest rates in May, with more reductions likely later in the year.

The UK jobs market is showing signs of strain. Vacancies fell to 781,000 in the first quarter, and payroll numbers also declined. Average pay rose 5.9%, but recent increases to National Insurance and the minimum wage are expected to weigh on employers. The unemployment rate held steady at 4.4%.

Trade tensions drag on European outlook.

Prospects for euro area growth have weakened as global trade tensions intensify. The region’s economy stagnated in April, with the services sector slipping back into contraction. Business confidence dropped to its lowest level since November 2022, hit by Trump’s tariff actions. Germany, the bloc’s largest economy, saw activity decline after three months of expansion.

Meanwhile, China’s economy grew 5.4% in the first quarter, fuelled by consumer subsidies and a rush of exports ahead of new tariffs. But the outlook is less certain as trade barriers bite. Without more government support, hitting China’s 5% growth target may prove difficult. Exports, which are responsible for a third of 2024’s growth, are expected to fall. Export shipments jumped 12% year on year in March, while industrial production rose 6.5% in the last quarter. But the struggling property sector continues to weigh on the economy.

Market-moving events

Tariffs return to centre stage. Tariff tensions intensified in April as President Trump announced a new wave of duties on Chinese imports, pushing the average tariff level to around 110%. The EU retaliated with tariffs on €26 billion of US goods, while China raised duties on select US imports to 125%. Markets were rattled by the renewed uncertainty.

Markets bounce on hopes of talks. Equity markets sold off sharply early in the month but

rallied after the US paused most tariff increases for 90 days and reports suggested negotiations

with China had resumed. Still, US GDP in Q1 2025 turned negative, dragged down by frontloaded

imports and weak personal consumption – the slowest since Q2 2023.

Growth outlook weakens, bonds disappoint. Surveys point to sluggish global growth in the second quarter of the year. As a result, investors are pricing in more rate cuts across developed markets. Credit spreads widened during April, but government bonds offered little of their usual protection, challenging traditional portfolio diversification.

Investment highlights

Portfolio rebalance and new positioning. We completed a full rebalance of OMPS portfolios in late April and transitioned to our latest 2025 Strategic Asset Allocation. This process ensures portfolios remain aligned with our long-term views and current economic expectations .

Tilt towards smaller US companies. We increased our allocation to the Omnis US Smaller

Companies Fund while reducing exposure to the Omnis US Equity Leaders Fund. US smaller companies trade on more attractive valuations and may benefit more from any improvement in domestic economic conditions, especially with the market concentrated in mega-cap names.

Adding to Chinese equity exposure. We also added to the Omnis Global Emerging Market Equity Leaders Fund, focusing on opportunities in Chinese equities. Policymakers in China are beginning to support the economy more forcefully, and many companies listed on Chinese markets have limited exposure to the US. This creates scope for recovery, particularly as domestic stimulus measures begin to take effect.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past performance should not be considered as a guide to future performance. The Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC are authorised Investment Companies with Variable Capital. The authorised corporate director of the Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC is Omnis Investments Limited (Registered Address: Auckland House, Lydiard Fields, Swindon SN5 8UB) which is authorised and regulated by the Financial Conduct Authority. — Approved by Omnis Investments on 1 May 2025

Comments