October market update - Equities rise despite economic headwinds

- Stefan Lubek

- Oct 6, 2025

- 4 min read

The US Federal Reserve cut rates for the first time this year against signs of a cooling labour market

Market strength.

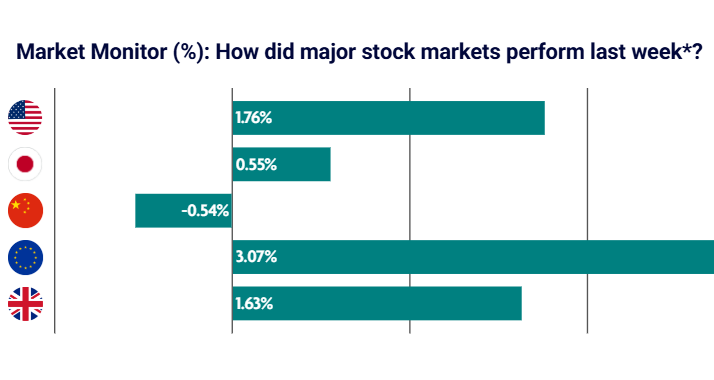

Global stocks were lifted after the US Federal Reserve (Fed) reduced interest rates by a quarter percentage point, bringing them down to a range of 4% to 4.25% – the first cut this year. It is the lowest level since early 2023, and Fed officials indicated that further cuts are likely in the months ahead.

Meanwhile, inflation has been creeping up. Since April, when Trump announced his reciprocal tariffs, inflation has risen from 2.3% to 2.9% in August. This is well above the Fed’s 2% target. After Trump’s tariffs took effect in August, most goods entering the US faced taxes of between 10% and 50%. Economists have warned that inflation could

become more pronounced in the coming months once companies start passing on the costs of tariffs to consumers.

The US economy remains resilient, even as the labour market shows signs of slowing. Just 22,000 jobs were created in August, bringing the total for the year to 598,000 – well below the 1.4 million recorded over the same period in 2024. Even so, unemployment is historically low at 4.3% and layoffs have been limited. Corporate earnings have also held up well, with more than 80% of companies surpassing revenue forecasts in the third quarter.

UK inflation holds steady.

It was a mixed month for UK stocks, with weak economic data dampening investor sentiment. UK inflation remains stubborn, holding at 3.8% in August, though food prices rose for a fifth consecutive month. The labour market is showing signs of weakening following April’s increase in employer National Insurance contributions, which analysts suggest has dampened hiring. Unemployment rose to 4.7% between May and July,

the highest level in four years.

The Bank of England held interest rates at 4% as it blamed the government for contributing to recent increases in inflation. It also announced it was scaling back the rate at which it is selling bonds into the financial market. The government is facing increasing pressure over its handling of the economy, with speculation mounting that tax rises could be announced in the Autumn Budget. Sluggish growth and rising borrowing costs have made it harder to meet fiscal targets.

Political instability in France.

France was thrown into a fresh political crisis after Prime Minister François Bayrou lost a confidence vote on the government’s debt-reduction plans. He was replaced by Sébastien Lecornu, a close ally of Emmanuel Macron.

Meanwhile, European stocks rallied in response to the Fed’s rate cut, with tech and bank shares leading. The European Central Bank (ECB) held its main policy rate at 2% for the third consecutive month. Annual inflation in the eurozone held steady at 2% in August. Eurozone business activity rose to its highest level in 16 months in September,

despite persistent economic weakness in France. Germany’s service activity picked up significantly, while job numbers remained flat.

China’s economy is showing signs of weakening amid strain from Trump’s trade wars, with factory output and consumer spending rising at their slowest pace for a year. Industrial output grew by 5.2% year on year in August, down from 5.7% the previous month, while retail sales expanded 3.4%, down from 3.7% in July. Deflationary pressures also persisted, with the consumer price index falling 0.4% from a year earlier after being flat in July. Even so, Chinese equities have continued to rally, supported by strong domestic household investment.

Market-moving events

US economic data remains mixed. Consumption is solid, but labour market signals are

weakening. Benchmark revisions and softer data have pushed the three-month average for job gains down to 29,000, below levels that would normally prevent unemployment from rising. In consumption-heavy economies like the US, higher unemployment could constrain spending and growth. It is unclear whether ongoing investment in AI can offset this softening.

Political uncertainty is rising. Angela Rayner has resigned as the UK Labour Party’s deputy leader, Japan is set to appoint its second Prime Minister within a year, and France has a new Prime Minister who may face a general election if the national budget fails to pass. Both France and the UK are facing fiscal constraints, which are only adding to geopolitical uncertainty.

US government shutdown. The closure is likely to dampen activity as furloughed staff delay spending. A further impact could be the delay of key labour market data from the Bureau of Labour Statistics. With signs of labour market weakness already evident, the

Investment Highlights

No changes in September. Following August’s rebalance of all OMPS portfolios, we made no changes in September.

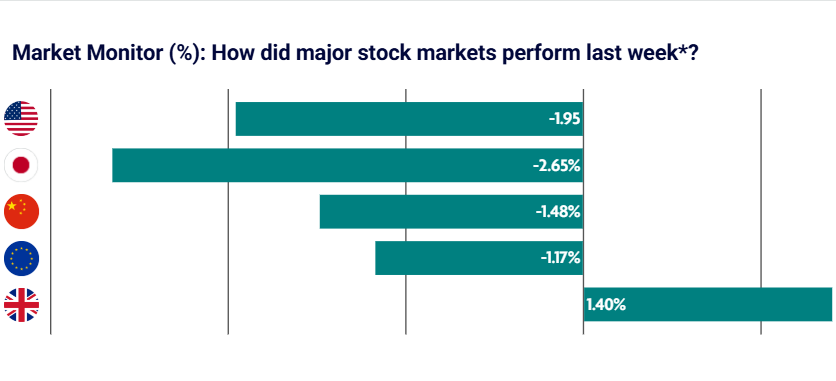

Risk appetite rewarded. Risk appetite was rewarded for the month, with global equities

performing strongly. Broad risk sentiment was assisted by the US Federal Reserve recommencing interest rate cuts. The strongest returns came from emerging markets and Asia (ex-Japan).

Remain cautiously positioned. We have a slight overweight in bonds and underweight in

equities. While equities continue to perform well, we are starting to see early signs of slowing economic growth, which could pressure equity valuations. We remain underweight the US due to a combination of high valuations and increased concentration risk. Our base case expectation of falling inflation, easing monetary policy and a soft-landing remains, although risks of a deeper recession remain elevated.

Issued by Omnis Investments Limited. This update reflects Omnis and our investment management firms’ views at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Past

performance should not be considered as a guide to future performance. The Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC are authorised Investment Companies with Variable Capital. The authorised corporate director of the Omnis Managed Investments ICVC and the Omnis

Portfolio Investments ICVC is Omnis Investments Limited (Registered Address: Auckland House, Lydiard Fields, Swindon SN5 8UB) which is authorised and regulated by the Financial Conduct Authority.

Approved by Omnis Investments on 1 October 2025

Comments