Omnis Investment Update: Focus on the Horizon

Friday 20th of March 2020.

Focus on the Horizon

As the coronavirus has continued to spread around the globe, financial markets have become increasingly turbulent. The S&P 500 index of US stocks has risen or fallen by 4% or more on each of the past eight trading days while volatility (as measured by the Vix index, otherwise known as ‘Wall Street’s fear gauge’) has surpassed that seen even at the peak of the financial crisis.

Navigating these stormy waters is undeniably challenging. However, we are reminded of the advice often given to sea-sick sailors: pick a point on the horizon and focus on it. For the Omnis Investment Team managing the Omnis Managed Portfolio Service (OMPS) portfolios, this means looking beyond the current turbulence and assessing the outlook for the coming months and even years. Once we focus on this point of the horizon, we believe shares – with many markets now appearing undervalued – offer compelling opportunities for patient investors.

A bear market in shares is often defined as a fall of 20% or more. By this definition, the current bear market is the sharpest on record. It took only 21 days for US shares to fall 20% - half the 42 days taken during the Great Depression in 1929 and more than ten times as quick as the descent from the pre-crisis peak in 2007. By any measure, recent market events have been of historic proportions.

The underlying reason for the turbulence in global financial markets is, of course, the continued spread of coronavirus around the world. Though China and South Korea – two early casualties of the outbreak – appear to have largely contained the virus, there is not yet enough evidence to suggest that this pattern can be repeated internationally. Governments around the world are implementing increasingly severe restrictions on their populations, but new cases continue to be reported at an alarming rate. Current expectations are for the new case rate to peak across Europe at some point over the summer.

Efforts to contain the virus are bound to have a significant impact on economic activity: a “technical recession” (two successive quarters of falling economic output) appears all but inevitable in the first half of this year. However, policymakers around the world have implemented – and, by all accounts, are continuing to develop – a raft of measures designed to ensure that this temporary economic slowdown does not evolve into something deeper and more protracted. Central banks have slashed interest rates and introduced measures designed to ensure global financial markets continue to function and ward off the threat of another financial crisis (see ‘Shades of 2008’ for further detail). Meanwhile, governments from Europe to Asia, the UK to the US, have pledged large sums to support businesses and workers that are impacted by efforts to counter the coronavirus threat. Success here will be measured by the extent to which increases in bankruptcies and unemployment are limited.

Despite the historic scale of the measures announced by central banks and governments, investors have thus far refused to countenance anything other than the continued spread of the virus and a significant economic downturn. Perhaps exacerbated by the challenges of translating a very human threat into something more quantifiable, fear has very much gained the upper hand on greed, and global stock markets have continued to lurch down. We believe this reaction may be overly pessimistic.

If the authorities succeed in containing the spread of the virus, and if increases in bankruptcies and unemployment are limited, we believe the measures being put in place by central banks and governments could fuel an exceptionally strong economic recovery in the second half of the year. Having fallen so sharply, we believe many global stock markets are now trading at valuations that do not reflect the potential for this scenario to unfold.

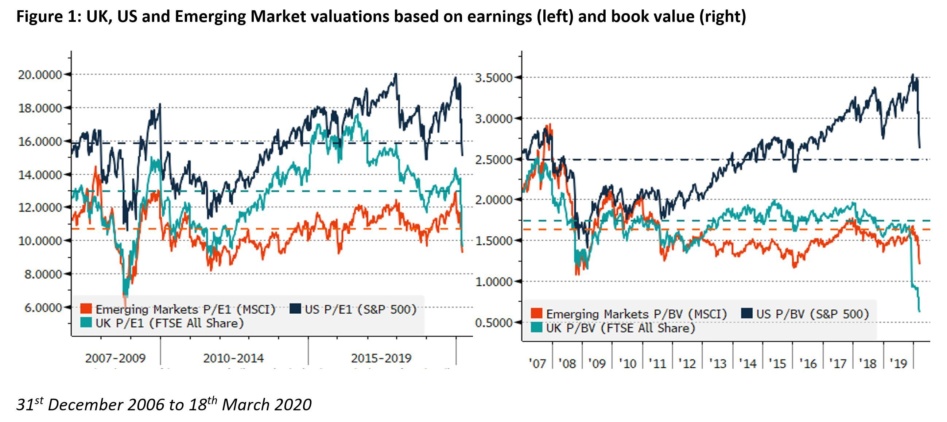

In the current environment, judging value on the basis of company profits is complicated by uncertainty over how the virus will impact those profits in the coming months. However, we can also value stocks on the basis of ‘book value’ (the value of a company’s assets such as its buildings, equipment and intellectual property). Book value tends to be more stable than profits and may therefore be more reliable in such turbulent times. On both measures, many stock markets – including those in the UK and emerging markets – are well below their long-term average valuations. Even the US stock market, which we have long considered expensive, is returning to much more reasonable levels (see Figure 1).

Our research shows us that starting valuations have a strong bearing on the future returns investors can expect from stocks. Historically, the lower valuations are when the investment is made, the greater the return that investment has delivered. The key to this relationship is a meaningful investment horizon. There is not much of a link between valuations and returns over days or weeks, but once you look to invest for a time measured in months or years the relationship becomes significant.

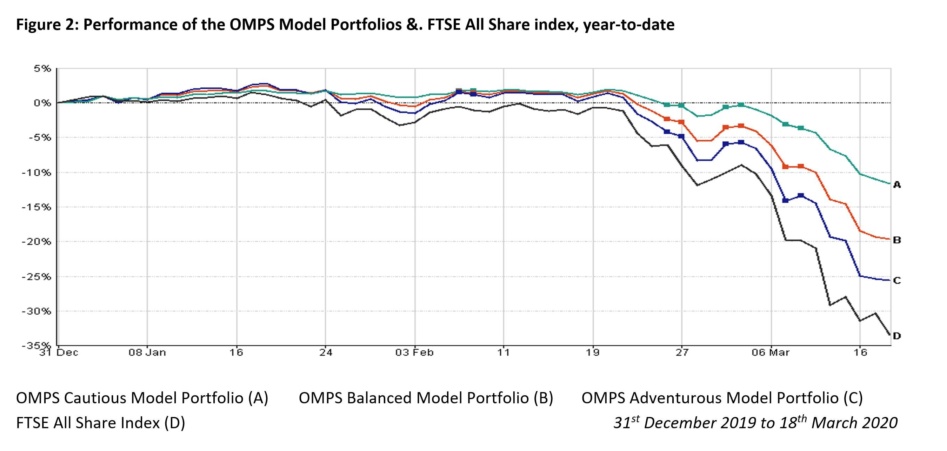

For those investors able to focus on an investment horizon that lies beyond the current market turbulence, we believe stock market valuations represent an attractive investment opportunity. Consequently, we have been patiently adding to our equity holdings as markets – and valuations – have moved lower (see Figure 2). Each pair of dots on the chart represents a change we have made in portfolios, first selling investments that have performed relatively well (typically bonds and alternatives) and then buying shares. We have so far made three of these trades as the stock market fall has intensified.

As markets have continued to move lower, our decision to add to shares has thus far not been rewarded. We do not aim for our trades to add value over periods of days or weeks, but over several months and even years. On this basis, we remain confident that adding to shares now will ultimately be rewarded.

While picking our point on the horizon may help us endure the current turbulence, we must ensure we are not at risk of being capsized by an unseen wave. What might this wave be? What might cause us to change course? Ultimately, our conviction rests on the expectation that the threat posed by the virus will recede over time, and that central bank and government policy will succeed in limiting the economic damage in the short-term and subsequently deliver a material boost to growth. We believe that stock markets are reflecting a much more pessimistic outlook than this. Signs that the spread of the virus is not slowing, or that bankruptcies and unemployment are rising sharply would challenge this conviction.

Though the exceptional current market conditions are undeniably challenging for all investors, we urge those who can to retain their focus on the long-term. While it is likely that we must endure more turbulence in the near term, we believe the longer-term opportunities for equity investors are compelling and continue to position portfolios accordingly.

Colin Gellatly

Deputy Chief Investment Officer, Omnis Investment

Issued by Omnis Investments Limited. This update reflects Omnis’ view at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your Openwork financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. The value of an investment and any income derived from it can fall as well as rise and you may not get back the original amount invested. Past performance is not a guide to future performance.

The Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC are authorised Investment Companies with Variable Capital. The authorised corporate director of the Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC is Omnis Investments Limited (Registered Address: Washington House, Lydiard Fields, Swindon, SN5 8UB) which is authorised and regulated by the Financial Conduct Authority.

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.